The Credit Wallet is a comprehensive solution for the origination, operation, and management of digital credit products. It is designed for fintechs, SOFOMES, originators, or B2B alliances seeking to operate simple lines of credit with integrated cards. The entire flow is 100% digital and scalable, adapted to projects that require speed of deployment, technical compliance, and proven user experience.

It allows for the implementation of both consumer credit models and agreement-based financing models (educational, payroll, affiliates), with direct integration with the Credit Bureau for scoring and card use (physical or digital) through Pomelo. It also includes complementary features such as service payments with MTCenter and automated notifications.

It has robust infrastructure for onboarding, validation, portfolio monitoring, risk control, and multichannel operations. Its modular architecture allows it to adapt to different business models without losing traceability or technical compliance.

Our Credit Wallet is designed to adapt to multiple origination scenarios, in both B2B and B2C environments. Below are the most common cases where it has been successfully implemented:

Digital originators focused on consumption: Platforms that grant personal loans to end users, either directly or through apps, marketplaces, or their own websites.

Educational, payroll, or affiliate financing:

Credit models linked to corporate agreements, education programs, employee benefits, or closed ecosystems.

Private label digital cards:

Fintechs or institutions seeking to issue digital credit cards under their own branding, controlling rules of use and credit limits.

SOFOMES or B2B alliances with mass onboarding: Financing schemes that require the integration of automated credit origination, assessment, and operation processes for large volumes of users.

Our Credit Wallet includes all the functional components necessary to operate simple credits securely, digitally, and audibly:

Digital origination flows:

Data capture, document validation, and application processing without human intervention.

Digital origination flows:

Data capture, document validation, and application processing without human intervention.

Integrated digital or physical card:

Card issued with Pomelo, ready to use from the approved balance.

Collection and tracking module:

Automated management of payment dates, notices, and reminders.

Portfolio dashboard and reports:

Visualization of portfolio behavior, delinquency, age, risk, and performance.

Compatible with SOFOM models or B2B alliances: Flexible architecture for integration with different legal entities or operating models.

Payment for services:

Integration with MTCenter to allow users to make payments directly from their credit line.

All versions share the same core and can be activated separately or in combination, depending on the business model, needs, and stages of the project.

Below is a detailed comparison of the main flows and modules available in each version of the Credit Wallet. This table serves as a guide for quickly visualizing what each variant of the base product includes, and how they are adapted to the customer's needs or operational approach.

Some modules are optionally activatable and can be included in multiple versions, depending on the use case and the configuration selected in each implementation.

Although both versions share a large part of the functional modules, their main difference lies in the Operational logic of credit:

The version of Simple Credit provides a non-revolving line, without a cutoff date or minimum payment calculation, designed for single uses or with fixed conditions.

The Credit card, on the other hand, operates under a revolving scheme, with a cutoff date, interest, reusable balance and automatic minimum payments.

Included by default

Available module, activatable by configuration or requirement

It does not apply or is not part of that version

The Credit Wallet is composed of independent modules that are activated depending on the version of the product (Simple Credit or Credit Card), the use case and the specific requirements of each customer. This modular architecture allows the solution to be adapted to different operating models, from digital originators focused on consumption, to B2B schemes with high scalability or programs with digital cards under their own brand.

Each module is developed with security, user experience and regulatory compliance standards, and can be visually integrated into the customer's brand without affecting business logic or the base infrastructure. The modules that are part of the product are described below, aligned with the comparative table of functionalities.

100% digital flow that allows users to create an account directly from the app, without human intervention. It includes the capture of personal data, scanning and validation of official documents using OCR, crossing with blacklists and acceptance of terms and conditions.

It meets compliance requirements to operate as a SOFOM or transmitter, but it can also be used in unregulated projects that require identity validation. It's designed to ensure traceability, fraud prevention, and a fast, frictionless onboarding experience.

Authentication module that allows you to log in using email and password. It includes options such as access recovery, session reminder, biometric authentication (Face ID or Touch ID) and automatic shutdown logic due to inactivity.

It is ready to scale to other security schemes such as OTP validation or second factor, depending on the risk levels defined by the customer.

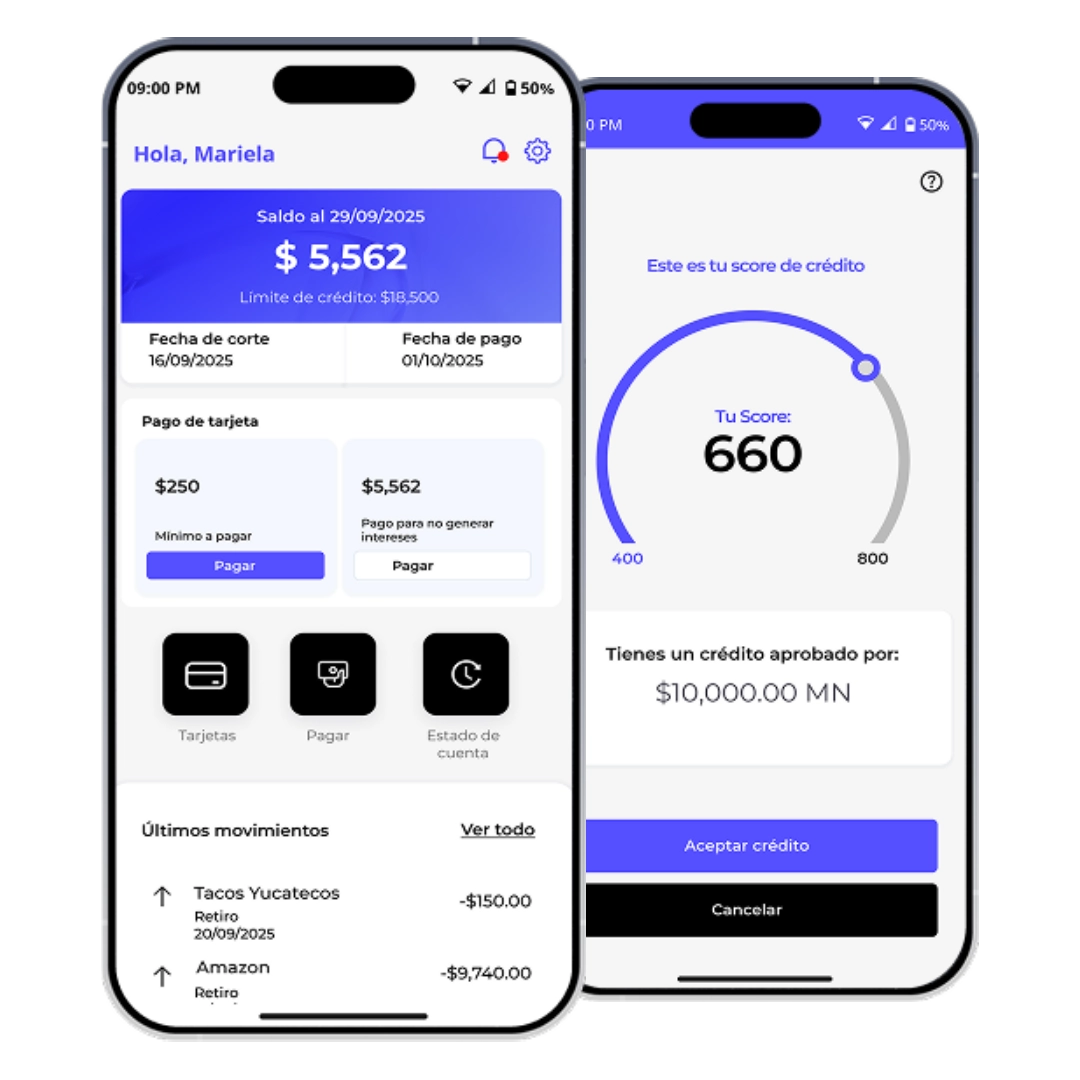

Main view where the user can check their available balance and a detailed history of movements. The list of transactions includes information by date, type of transaction, amount, and status.

It can adapt to the customer's branding and scale in functionality as required (adding filters, categories or integration with external tools).

Automatic generation of alerts for key events such as unusual movements, processed payments, rejections or security changes. Alerts can be sent via push, email or displayed within the app.

The notification channels and rules are configurable, allowing them to adapt to more or less strict risk models, depending on the type of credit operated.

Functionality that allows you to make payments to public and private services directly from the available balance in the wallet.

It includes validation of references, display of the name of the service and confirmation of the amount before shipping.

The system allows you to operate with single or scheduled (recurring) payments, and offers a simple payment experience aligned with what the user expects from a banking app.

It is integrated with MTCenter as a network provider, allowing access to a wide range of services nationwide.

This module can be enabled as a dedicated section or embedded within other flows depending on the customer's needs.

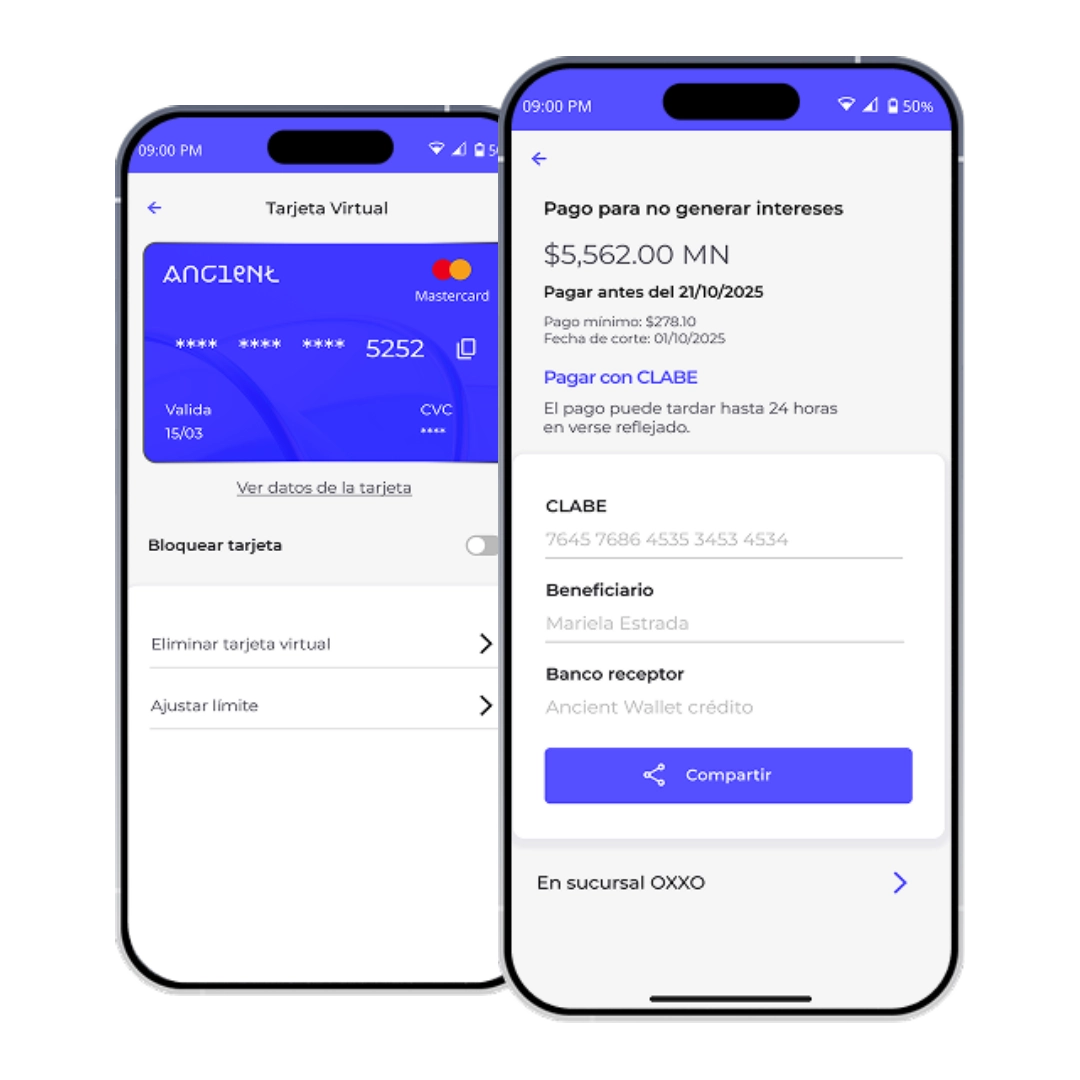

It allows you to manage a card (digital or physical) issued by Pomelo and linked to the user's credit account. The functions include activation, blocking, querying sensitive data, PIN and associated movements.

The integration with Pomelo ensures traceability, control and compliance with the customer's operational or regulatory requirements.

Permite definir y mostrar al usuario el monto total de su línea de crédito, el saldo disponible y los montos utilizados. El valor asignado puede ser fijo o dinámico, según el perfil del usuario o el tipo de crédito.

Module that performs queries to Credit Bureau to validate the user's financial behavior and feed a process of configurable scoring.

It generates and shows the user their account statement, including the details of the movements, line used, payments made, interest and cutoff date. It is essential for credit card schemes or programs with recurring dispersion.

It can be included in the app as a dedicated section or delivered by other means, depending on the operating model.

Module that automatically calculates the minimum payments required and, if applicable, the total amount to be paid to avoid interest. This calculation can be adapted to different schemes: revolving credit, dynamic rates or customized plans.

It includes validations, simulations and clear visual communication for the user.

Flow that allows you to schedule payment collection on key dates, send reminders and make automatic payment attempts using SPEI, direct debit or payment links.

The system records each collection attempt and can be integrated with tracking strategies, notifications or monitoring panels.

Flow that allows the user to close their account directly from the app.

It includes identity verification, confirmation of intent, cancellation of associated products and disengagement of sessions or devices.

It also makes it possible to record the reason for cancellation for subsequent analysis or statistical purposes.

This module is designed to run without friction, but with the necessary controls to prevent accidental or malicious closures.

From this section, the user can view and update their personal and contact details, such as email, telephone number and password.

Each flow is guided by intuitive screens, with step-by-step confirmations and validations.

It also allows you to configure general account options, such as beneficiaries, language, notifications and other settings.

It is a key module for keeping data updated and reinforcing the user's sense of control over their account.

Security module that allows the user to see all devices with an active session and manage access. It includes the ability to close remote sessions.

This module reinforces the app's perception of security, reduces operational risks and is especially useful in contexts where multi-device access is enabled.

Functionality available for physical card programs, allowing ATM withdrawals with PIN validation and configurable limits. The withdrawal is charged directly to the available line of credit.

This module is useful in programs with dispersion in areas with low banking or where immediate liquidity is required.

Module focused on providing direct and multichannel service to the user. From this section, the user can access:

- Frequently Asked Questions (FAQ)

- WhatsApp channel

- Contact by email

- Direct call option

It is designed to scale requests based on urgency and offers a simple interface to activate each contact channel.

Brand personalization, user experience and flows

We adapt the interface, texts, colors, logos and product names to your brand identity. Operational flows (such as onboarding, scoring or payments) are also customized to respond to your business model and internal policies.

Production-ready cloud infrastructure

The environment is deployed on scalable, secure and highly available infrastructure. It includes environments separated by environment (dev, QA, production), monitoring tools and backup policies. It is delivered completely ready for operation.

Mature technology, already in production with customers

Reales in Mexico

This product is not an MVP. It is based on proven infrastructure, auditable operating flows and processes that already operate with real volumes in the Mexican market.

Full source code, without blocks or revenue share

We do not operate under restrictive schemes or abusive licensing. Complete code is delivered, with documentation and without closed dependencies or usage or volume fees.

Modular and customizable architecture

Each component of the system functions as an activatable or deactivatable module depending on the customer's needs. This allows you to implement only what is necessary for each version of the product, without burdening with functionalities that will not be used.

Fast go-to-market: weeks, not months

The model is designed to be integrated and implemented in weeks. This allows you to quickly validate the market, iterate with real customers and reduce time to market without sacrificing technical robustness or regulatory compliance.

Ancient delivers the wallet with an infrastructure of tested and functional integrations.

Integration requests with different vendors involve additional effort and must be technically evaluated.

The integrations are interchangeable thanks to a decoupled architecture, but they require additional development effort if they are not within the base stack.